Mortgage Market Update February 26, 2025

Back

27 February 2025

Mortgage Market Update February 26, 2025: Rates have moved lower… but do we have the economic data to trust the drop is here to stay?

I’m going to keep this market update short and sweet as the story for March rates will be told by Friday’s upcoming January PCE Price Index report. However, as we’ve finally witnessed some mortgage rate drops in the past few weeks (I love it!), I wanted to push out a few helpful analytics heading into Friday’s report as there is a chance this may be short-lived.

Stock Losses Contribute to Mortgage Rate Decrease

You’ve heard me say it before and I’ll say it again: The single biggest leading indicator of long-term mortgage rate movements will be inflation data. Why is this? This is very important to understand and justifies my position that the only data that matters is inflation data when it comes to predicting long-term rate movements. Inflation devalues long-term bonds. When inflation rises, the fixed interest payments a bond provides to the investor become less valuable. This makes the bond less attractive to the investor compared to new bonds issued at higher interest rates. This is why mortgage rates move higher, not lower, in response to higher inflation data.

Yet somehow despite the stubborn inflation data we’ve received thus far in 2025, we find ourselves in the lowest mortgage rate environment since mid-December 2024. This is due to a variety of complex factors, including recent stock market losses stemming from concerns regarding tariffs and a weaker-than-expected S&P PMI report last week. S&P PMI is a broad index that tracks business activity in the services sector.

It’s important to note that stocks and rates don’t always move in concert. In fact, when stocks are reacting to Fed policy, they often move in the opposite direction from rates. This too can make predicting mortgage rate movements very tricky. But when stocks are selling for their own reasons and when that sell-off is large, investors will often seek safer waters in the bond market, thus pushing rates lower. This has brought us lower mortgage rates for at least the short term.

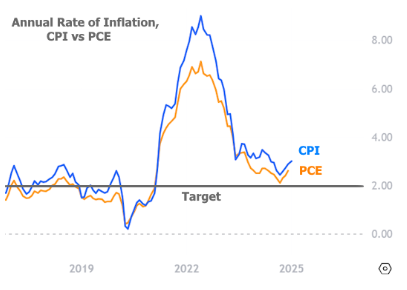

Fingers Crossed for January Core Personal Consumption Expenditures (PCE) Report Due Friday 2/26

The Core PCE report matters for interest rates because it is the Federal Reserve’s preferred measure of inflation. The Fed uses Core PCE to gauge underlying inflation trends, as it excludes volatile food and energy prices, providing a clearer picture of broader price pressures.

According to current forecasts, the January Core PCE estimates for Friday’s report is expected to be .35% month-over-month, with a year-over-year increase of 2.64%. If it comes in as forecasted, this would mean a slight decrease in the previous month’s annual rate of 2.8%. These forecasts were adjusted after last month’s hotter-than-expected numbers, and underscores the ongoing struggle to bring inflation fully under control.

While these figures certainly mark a decrease from the peak inflation numbers of 2022 and 2023, this month’s report will be critical in assessing whether inflation is continuing to make progress towards the Fed’s 2% target. If it remains stubbornly elevated, it’s reasonable to assume we will see long-term rates respond accordingly Friday.

Back to Blogs